New regulations have been issued for the legal regulation and regulation of electronic cigarettes, which will be listed as taxable consumer goods and subject to consumption tax!

Since November 10th of last year, electronic cigarettes have been officially included in the "Regulations on the Implementation of the Tobacco Monopoly Law" for regulatory purposes. Since implementation with reference to relevant regulations on cigarettes, relevant departments have successively issued a number of new regulatory regulations, proposing a series of specific measures for the regulation of electronic cigarettes. Recently, the Ministry of Finance, the General Administration of Customs, and the State Administration of Taxation jointly issued the "Announcement on the Collection of Consumption Tax on Electronic Cigarettes" (No. 33 of 2022, hereinafter referred to as "Announcement 33"), stipulating that the consumption tax shall be levied on electronic cigarettes as of November 1, 2022. This article provides a brief introduction to the new regulations on the regulation of electronic cigarettes, the background of the collection of consumption tax on electronic cigarettes, and a detailed interpretation of the regulations on the collection and management of consumption tax on electronic cigarettes from the perspective of the six elements of taxation, in order to help taxpayers of consumption tax on electronic cigarettes operate in compliance with the law and effectively address tax risks.

1、 New regulations on the legal and chemical regulation of electronic cigarettes

On June 1, 2021, the newly revised "Law on the Protection of Minors" explicitly stipulated, for the first time, in the form of a national law, that "the sale of electronic cigarettes to minors is prohibited.".

On November 10, 2021, the "Regulations for the Implementation of the Tobacco Monopoly Law" was revised and implemented, specifying that "new tobacco products such as electronic cigarettes shall be implemented in accordance with the relevant provisions of these Regulations on cigarettes." Accordingly, electronic cigarettes were officially incorporated into the tobacco regulatory system and a monopoly management system was implemented.

On May 1, 2022, the "Measures for the Administration of Electronic Cigarettes" came into effect, clarifying the definition of electronic cigarettes and making specific provisions for the production, sales, transportation, import and export, supervision and management of electronic cigarettes within China.

On October 1, 2022, the "Compulsory National Standard for Electronic Cigarettes" (GB 41700-2022) was implemented to provide technical support for the electronic cigarette regulatory system. According to this mandatory standard, the nicotine content of e-cigarettes should not exceed 2%, whereas most e-cigarettes on the market previously had a nicotine content of 3% or 5%.

On October 31, 2022, seven departments, including the State Administration of Market Supervision and the Central Cyberspace Information Office, jointly issued the "Guiding Opinions on Further Standardizing Star Advertising Advocacy Activities", which explicitly stated that stars should not advertise for tobacco and tobacco products (including electronic cigarettes).

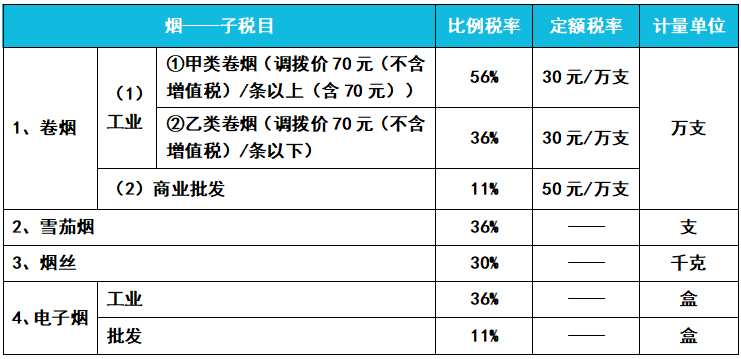

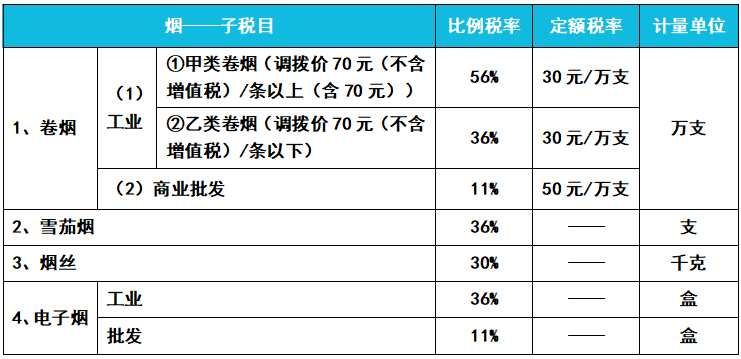

On November 1, 2022, according to Announcement No. 33, electronic cigarettes were included in the scope of consumption tax collection, and the consumption tax was levied at an ad valorem rate of 36% and 11% at the production and wholesale double links, respectively.

2、 Background of levying consumption tax on electronic cigarettes

Consumption tax is an important tax source in China's current 18 major taxes, second only to value-added tax, corporate income tax, and individual income tax. In recent years, with the reform of individual income tax, consumption tax has surpassed individual income tax several times to become the third largest tax. The main function of consumption tax is to regulate rather than finance revenue. Therefore, consumption tax is selectively levied, only on explicitly listed taxable consumer goods. There are currently 15 categories of taxable consumer goods in China, including cigarettes, alcohol, firecrackers, fireworks, high-end cosmetics, refined oil, precious jewelry, jewelry, jade, golf balls, and ball gear, high-end watches, yachts, wooden disposable chopsticks, solid wood flooring, motorcycles Cars, batteries, coatings, etc.

From the perspective of the structure of China's consumption tax income, the two main sources are tobacco and refined oil, respectively. Prior to Announcement No. 33, the taxable consumer tobacco category in the "Taxable Consumer Product Name, Tax Rate, and Measurement Unit Comparison Table" included three sub categories of cigarettes, cigars, and tobacco. Based on the management of electronic cigarettes by referring to cigarettes, electronic cigarettes should also be included in the scope of taxable consumer goods.

According to statistics, China is the world's largest e-cigarette production base, with exports accounting for 90% of the world's total output. In 2021, China's total e-cigarette exports reached 138.3 billion yuan; According to estimates, the annual sales revenue of the domestic electronic cigarette market is about 20 billion yuan.

In view of the above reasons, Announcement 33 states that "in order to improve the consumption tax system, maintain a fair and unified tax system, and better play the role of consumption tax in guiding healthy consumption," a consumption tax is imposed on electronic cigarettes.

3、 Six Elements of Electronic Cigarette Consumption Tax Collection and Management

From a tax perspective, the collection and management of a specific tax category is usually analyzed through six elements: taxpayer, tax object, tax rate, tax reduction and exemption, tax link, and tax period. Below, we will interpret the consumption tax on e-cigarettes through the six elements detailed explanation announcement No. 33.

(1) Taxpayer

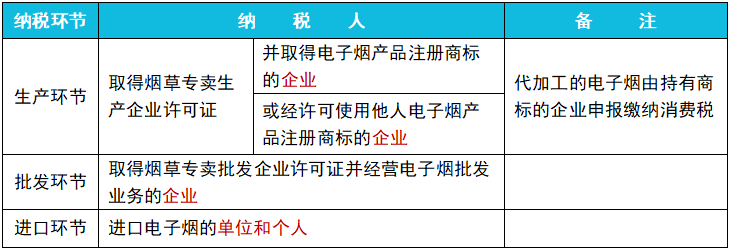

Taxpayers, also known as taxpayers, are entities and individuals that are directly obligated to pay taxes under the law, which is commonly referred to as taxpayers. Article 2 of Announcement No. 33 stipulates that "entities and individuals that produce (import) and wholesale electronic cigarettes within the territory of the People's Republic of China are consumption tax taxpayers." It further stipulates the methods for determining taxpayers under different circumstances.

It should be noted that there are differences in the tax declaration between the commissioned processing of e-cigarettes and the commissioned processing of other taxable consumer goods. The commissioned processing of e-cigarettes refers to "the consignor's own declaration of tax payment" rather than "the consignor's collection and payment on behalf of the consignor.". Article 4 of the "Provisional Regulations on Consumption Tax" stipulates that "for taxable consumer goods that are commissioned for processing, unless the commissioned party is an individual, the commissioned party shall collect and remit taxes upon delivery to the commissioned party."; According to Announcement No. 33, "If electronic cigarettes are produced through agent processing, the enterprise holding the trademark shall pay the consumption tax." The Interpretation of the Announcement of the State Administration of Taxation on Issues Related to the Collection and Administration of Consumption Tax on Electronic Cigarettes by the State Administration of Taxation further clarifies that if electronic cigarettes are produced through agent processing, the enterprise holding the trademark shall declare and pay the consumption tax.

Accordingly, if the enterprise is only engaged in the business of processing e-cigarette products on a commission basis, it is not a consumer tax payer for e-cigarettes. It should be noted that the quantities of "OEM" and "self produced and self sold" should be accounted for separately, otherwise full tax payment will be made.

(2) Tax payee

The object of taxation is the object of taxation specified in the tax law, and the object of consumption tax collection is taxable consumer goods. Tax items are the concretization of tax objects, such as consumption tax items, which are classified into the aforementioned 15 categories and can be further subdivided into tax items.

Announcement 33 states that an electronic cigarette item will be added under the tobacco tax item, and the object of the electronic cigarette consumption tax is electronic cigarette products, including cigarette bombs, cigarette sets, and electronic cigarette products sold in combination with cigarette bombs and cigarette sets. According to the mandatory national standard for Electronic Cigarettes (GB 41700-2022), electronic cigarettes refer to electronic transmission systems used to generate aerosols for human consumption, including cigarette bombs, cigarette sets, and electronic cigarette products sold in combination with cigarette bombs and cigarette sets. Smoke bombs refer to electronic cigarette components that contain aerosols. Cigarette is an electronic device that atomizes aerosols into inhalable aerosols.

Tax calculation basis is another concept related to the object of taxation, which is the standard or basis for calculating specific tax amounts. According to Announcement No. 33 and relevant regulations: (1) Enterprises engaged in the production and wholesale of electronic cigarettes should use the sales volume of the production and wholesale of electronic cigarettes as the taxable price; (2) "Where a manufacturing enterprise sells electronic cigarettes by way of consignment, the taxable price shall be the sales amount (including the full price and extra price fees collected) sold by the distributor (agent) to the electronic cigarette wholesale enterprise;"; (3) The import of electronic cigarettes shall be calculated and taxed according to the component taxable price; (4) For manufacturers that produce and use electronic cigarettes for their own use and do not have a sales price for similar consumer goods, it is necessary to calculate the composite tax price based on the cost profit margin. The State Administration of Taxation has tentatively determined that the national average cost profit margin for electronic cigarettes is 10%.

It should be emphasized that taxpayers engaged in the processing business of electronic cigarettes in the production process of electronic cigarettes should separately account for the sales volume of electronic cigarettes with trademarks and the sales volume of electronic cigarettes processed on behalf of them; If not separately accounted for, the consumption tax shall be paid together.

(3) Tax rate

Electronic cigarettes are taxed on an ad valorem basis. The tax rate for production (import) is 36%, and the tax rate for wholesale is 11%.

(4) Tax reduction and exemption

China is the world's largest e-cigarette production base, with exports accounting for 90% of the world's total output. We implement a policy to encourage the export of e-cigarettes. Therefore, when taxpayers export e-cigarettes, the export tax refund (exemption) policy is applicable, and e-cigarettes are added to the list of non-taxable imports from the border trade and taxed according to regulations.

The collection of consumption tax on imported electronic cigarettes carried by individuals is summarized as follows in accordance with the Announcement on Issues Related to the Taxation of Electronic Cigarettes issued by the General Administration of Customs on October 27, 2022:

(5) Tax payment process

The tax payment link of the consumption tax on electronic cigarettes is a double cycle tax on production (import) and wholesale. There is a significant difference between value-added tax and the whole chain of taxation.

(6) Tax period

The tax payment deadline is the legal deadline for taxpayers to pay taxes to the state. Overdue tax payment will bear a late fee. The forms of tax payment period in China include regular tax payment, one-time tax payment, annual tax payment, installment prepayment, or payment. According to the Provisional Regulations on Consumption Tax, the tax payment periods for consumption tax are 1 day, 3 days, 5 days, 10 days, 15 days, 1 month, or 1 quarter. The specific tax payment period of a taxpayer shall be determined by the competent tax authority based on the size of the tax payable by the taxpayer; "If the tax cannot be paid within a fixed period of time, it may be paid on a per occurrence basis.". Taxpayers who import electronic cigarettes shall pay the tax within 15 days from the date when the customs fills in and issues the special payment form for customs import consumption tax.

4、 Prompt

Given that e-cigarettes are a new consumption tax subcategory, they will be levied as of November 1, 2022. In order to prevent taxpayers of e-cigarettes from having a poor understanding of policies regarding tax declaration and other matters, which may lead to tax risks, it is recommended that taxpayers take the initiative to consult with the tax authorities and handle the identification of consumption tax categories, in order to smoothly carry out tax declaration and other related tax-related matters. At the same time, enterprises entrusted with the processing of e-cigarettes should improve their financial systems and independently account for the sales of their own trademark e-cigarettes and the sales of the processing e-cigarettes on behalf of them, to avoid increasing the tax burden.

Related recommendations

- Tax lawyers review the draft of the revised Tax Collection and Administration Law for soliciting opinions

- New Measures for Punishing "Dishonesty" by the Supreme People's Court at the Two Sessions in 2025 (Part 3): "Height Limit" Single Release Mechanism

- New Measures for Punishing "Dishonesty" by the Supreme People's Court at the Two Sessions in 2025 (Part 2): Grace Period System

- Interpretation of the Management Measures for Compliance Audit of Personal Information Protection - Feeling the Rhythm and Rhythm of Regulatory Flow